Abstract: The recent

growth of the new governance indicators requires a discussion about

misconceptions when transposing means and goals of business administration to

the public sphere. For this purpose, the public value theory can provide a

neutral perspective for current studies on public governance, which implies the

need for reassessing some of the former indicators. In this paper, we

demonstrate the feasibility of this theoretical construction and propose a

quantitative multidimensional indicator for the state-level public finance in

Brazil. Based exclusively on the fulfillment of legal requirements, a 15-year

sample of all Brazilian states brought results different from the previous

findings. They revealed that the quality of governance is uncorrelated with

wealth, breaking the inequality assumption that rich states perform better than

the poor ones.

Keywords: Public Governance;

Public Finance; Governance Indices; Public Value.

Resumen: La reciente proliferación

de nuevos indicadores de gobernanza hace necesaria una discusión sobre

conceptos erróneos al transponer los medios y objetivos de la administración de

empresas a la esfera pública. En este escenario, la teoría del valor público

puede proporcionar una perspectiva neutral para los estudios actuales sobre la

gobernanza pública, lo que implica la necesidad de reevaluar algunos de los

indicadores anteriores. En este trabajo, demostramos la viabilidad de esta

construcción teórica y proponemos un indicador cuantitativo y multidimensional

para las finanzas públicas a nivel estatal en Brasil. Basado exclusivamente en

el cumplimiento de los requisitos legales, una muestra de 15 años de todos los

estados brasileños arrojó resultados diferentes a los hallazgos anteriores.

Revelaron que la calidad de la gobernanza no está correlacionada con o nivel de

riqueza, rompiendo el supuesto de desigualdad de que los estados ricos

funcionan mejor que los estados pobres.

Palabras clave: Gobernanza pública;

Finanzas públicas; Índices de Gobernanza; Valor Público.

Resumo: A recente proliferação

de indicadores de governança reconduz à discussão acerca da transposição de

meios e fins da administração de empresas para a esfera pública. Neste cenário,

a teoria do valor público pode fornecer uma perspectiva neutra para os estudos

atuais sobre governança pública, implicando na necessidade de reavaliação de

alguns indicadores previamente elaborados. Neste artigo, demonstramos a

viabilidade dessa construção teórica e propomos um indicador quantitativo e

multidimensional para as finanças públicas estaduais no Brasil. Com base

exclusivamente no cumprimento de requisitos legais, uma amostra de 15 anos de

todos os estados brasileiros trouxe resultados diferentes dos achados

anteriores. Eles revelaram que a qualidade da governança não é correlacionada

com a riqueza, quebrando a suposição de desigualdade de que os estados ricos

têm um desempenho melhor do que os estados pobres.

Palavras-Chave: Governança Pública;

Finanças Públicas; Índices de Governança; Valor Público.

Introduction

During the second half

of the 20th century, Latin American countries and governments faced several

social and economic difficulties. After the democratic transition, the recently

established democratic governments were pushed by their citizens to play more

active roles in economy, taking into account social aspects and the redistributive

functions in their activities. On the other hand, they were not able to increase

their public spending, given their inability to raise taxation levels (Tanzi,

2008).

Due to evident exposure

to European influences, these countries have developed policies that protect

individuals “from the cradle to the grave”. Although the extension of this

assistance may vary within each region, these programs usually include public

pensions, public health programs, free public schools, subsidies to large

families, unemployment compensation, support for disabled people, and public

housing (Tanzi, 2008, p.9).

The recent pursuit of better

private managerial methods, roughly applied to public services, increased the

perception that the public sector staff does not have the ethos they

once had. This idea might be associated with the narrow focus on performance

indicators, the lack of responsiveness to public value concepts, and the

failure to assess the impact of the service deliverance on the communities

(Blaug, Horner and Lekhi, 2006, p.26).

In a context of significant

social and economic inequalities, Brazil is currently exposed to a widespread

discourse of good governance, and policies and managerial models, whose results

do not seem to be positive though – at least for the population. In order to

tackle this issue, it is fundamental to revisit the origins of a genuine governance

for the public resources, and then draw the bases for indicators and subsequent

indexes, to measure what they propose: governance in public administration

(Hood, 2012).

In addition to that, the

welfare of the citizens of a country is linked to values of socio-economic

indicators. Governments try to influence them through their spending policies,

indicating the pursuit of a public value notion.

This paper estimates a

governance indicator by using budgetary and financial variables to evaluate the

governmental performance, according to the public value perceived by citizens.

It provides a new tool for state-level governments to assess their financial

performance. On that account, it works as “a measurement framework (...) [that]

enables politicians, managers and the public to recognise when and the extent

to which such value is being created.” Furthermore, it contributes to the

advance of knowledge by expanding the theoretical comprehension of public

value, quantitatively applied to subnational governments in Brazil. (Blaug et

al., 2006, p.60).

This article is divided

into five parts. The first one is the introduction, which is followed by a theoretical

framework. The third part comprises the methodology for the indicator assessment,

and the fourth presents the results and main achievements. Finally, in the

fifth section, we conclude and offer some final remarks.

Theoretical Background:

Public management is a

topic often approached in papers on organizational theory and economics, but little

mentioned in finance studies. As this paper establishes a cutoff point between

private managerial methods and commonly discussed public service theories, it

seems proper to review the most traditional theories, and if and when they are applied

to public finances. The following sections examine central aspects of some of

the recently adopted theories and conclude that they are useful for Brazilian

studies on the public sector. We expect the reader to assume that we do not

endorse any particular point of view as right or wrong. On the contrary, they

can complement each other to develop the public administration.

From the Hobbesian government

to the rule of law in a fiscal state: the reason for public finance rules

The Hobbesian writings

assert that a government, or any authority, is the only alternative to anarchist

chaos, or natural state, via monopolization of the use of coercive power,

avoiding the war of all against all. For that reason, a State should

have the freedom of a coercive power in the hands of a sovereign, and the

complete freedom would be named order (Hobbes, 1651/1998; Brennan,

Buchannan, 1980).

The Hobbesian approach to

coercive power can be divided into two different branches. The first one, from

now on referred as the fiscal state, derives directly from the means necessary to

fund this state, “concerning the treasure, as tributes, impositions, rents,

fines, or whatsoever public revenue, to collect, receive, issue, or take the

accounts thereof” (Hobbes, 1651/1998, p.341). Brennan and Buchanan (1980, p.

11) argue that, for an ordinary citizen, “the power to tax is the most familiar

manifestation of the government’s power to coerce” and involves the imposition

of charges that are only fulfilled by transferring economic resources to the government.

In addition, Oliveira (2009) highlights that any attempt to measure the economic

and social effects of the fiscal policy should consider the mechanisms that the

state uses to obtain resources; the force of the government-governed

relationship, as people provide the state with the power to tax; and the

principles that guide the loss distribution among taxpayers, as well as the

benefits for the whole society (Oliveira, 2009, p.81).

The second branch, which

we nowadays call the rule of law, is the indistinct application of the rules to

the ruled ones. Despite Hobbes’ arguments against the inclusion of the state

(or the sovereign) in the rule of law, the later evolution of this idea,

especially after Kant, led to the conclusion that the state has the moral

obligation to obey it, at least.

The rule of law can be

defined as a publicly available written law, promulgated by an authority before

the events that it regulates, and fairly applied to relevant state institutions,

including the judiciary. By fairly, it should be understood that the law

must have similar effects for equivalent cases, regardless of the class,

status, power, or any other attributes of each one of the parties involved. It

should also allow each party to be equally voiced (O’Donnell, 2004, p.33). Any

eventual deviance from this standard might indicate the absence of the rule of

law, sometimes replaced by cases constructed as ruled by law. Two

possibilities arise from this scenario. The first one is the violation of the

international moral standards that countries are pushed to agree to and write

in their constitutions. The second is the disrespect for a fundamental notion

of fairness and equity, according to which, cases alike should not have

different consequences; otherwise the responsible authorities would not feel

obligated to make similar decisions in future occasions (O’Donnell, 2004,

p.34).

Furthermore, Fuller

broadens the definition of the rule of law to a moral issue, enforcing the

congruence between the official action and the declared rules. In other words,

“the respect of citizens and the state for the institutions that govern […]

social interactions among them” is referenced as one of the branches of

governance.(Kaufmann, Kraay, Mastruzzi,

2011, p.222).

About public governance

On the second half of

the 20th century, governance emerged as a critical challenge for academics. The

post-Second World War context and the transformation of the former western

welfare conception required a new comprehension of the theory, practice, and

dilemma of the new societal construction and its “constantly shifting and

contingent nature of practical political activity” (Zumbansen, 2012; Bevir,

2010, p.11).

When applied to public

issues, governance can be defined as the formal and informal arrangements that shape

public decision-making. It can also be understood as the way public actions are

guided, in a perspective of keeping constitutional values, in the face of constantly

changing problems, environments, and agents (OECD, 2005, p.16).

Policy-makers widely use

the term governance in the attempt to improve the living conditions of people in

poverty and oppression situations. Due to its ambiguity, the concept can be

easily reshaped according to the preferences of each author. In this sense, one

must be aware that, while the understanding of governance may be enhanced, the extent

of uses can obfuscate its meaning (Peters, 2012). In its original form, governance

refers to the “collective choices that cannot be addressed adequately by

individual action”, and the search for proper means to make decisions. Thus, governance

embeds some accountability concepts, once the agents involved in this

decision-making are supposed to be held accountable for the actions. (Peters,

2012, p.20).

Chan and Xiao (2009) mention

that financial management is a critical point for assessing a government’s

ability and capacity to deliver services (and by extension, goods, according to

Musgrave’s definition). So, a financial manager is responsible for keeping “a score

of finance-related exchanges, advis[ing] management on the terms of those

exchanges, and monitor[ing] financial performance of all the parties concerned”,

and for watching the viability of the institutional network and its

participants, including contractual performances (Chan and Xiao, 2009, p.115).

Feldman and Khademian

(2002) propose an alternative view on the governance issue. In contrast to the

principal agent relations, they discuss the structure of the interactions

between the parts, which are determined by constitution, statutes, custom, and

practice. These principal-agent relations determine what actions are enabled or

constrained. In other words, they regulate who can participate in the decision-making.

From this point of view

“the public

manager’s responsibility rests not only with the policy outcomes, but making

visible and continuously evaluating the appropriateness of the nature and

quality of the relationship structures they create and recreate through their

actions” (Feldman and Khademian, 2002, p.545)

As a financial extension

of the governance model, Stoker (2006) defines the public value management paradigm

as a thesis-antithesis-synthesis result from the previous new public financial management,

but with the comprehension of its narrow utilitarianism.

In order to put the

public management principles back to action, Stoker (2006, p.47) reminds us that

public affairs are considerably different from the commercial sector

activities. As “governing is not the same as […] buying and selling goods in a

market economy”, some of the prescriptions of the new public management are not

appropriate to a public experience.

To challenge the traditional

public administration and new public management, public value is defined by

Constable, Passmore, and Coats (2008) as a broad approach to thinking about

public administration and continuous improvement in public services. For this study,

we chose to follow the original perspective of Moore (1995), which accepts a

concept of value more extent than the economic sense, and which is appraised according

to what citizens consider valuable.

This evaluation requires

the public to participate in the decision-making processes, in a representative

democracy enabled by the managers. They shall facilitate this procedure by developing

powers and emphasizing the representative role of the elected members, thus gaining

strength from the active involvement of the community (Blaug et al.,

2006, p.19). According to Moore (2003), “the ultimate value [...] can be

measured by the satisfaction and benefits it delivers to its clients, or by the

social results that it produces for the society at large”. As an additional

note, these organizations should satisfy their customers, or citizens, in the

case of public entities, and help them to change their lives and achieve the

desired social outcomes.

As Blaug et al. (2006)

remark, although goal-directed models have brought an image of rational

management to government organizations, they often ignore the impacts on

operational activities. This negligence requires the use of a multi-dimensional

approach to measuring performance in the public sector (Blaug et al.,

2006, p.56; Modell, 2004).

In spite of all

traditional methods of measuring government performance, Blaug et al.

(2006) remind us of this:

“the goal of

public management in a public value framework is to ensure that organisations

are more responsive to what the public wants and needs. […] In this respect, it

moves away from narrow conceptions of performance management or economic

evaluations that attempt to sum the social, economic or environmental impact of

an institution, towards an analysis of the capacity of organisations to deliver

public value”. (Blaug et al., 2006, p.56).

The capacity, however,

should be defined within the framework proposed by Matthews (2012). According

to the author, the governance approach, in its third wave, highlights “the

prevailing influence of governing norms and traditions, and how they have

affected the capacity of states to respond to the challenges associated with

the governance narrative” (Matthews, 2012, p. 282).

More than a simple

definition, the public value also provides a “guiding concept” for theorists

and practitioners of public administration. Among the many definitions it has gained

in the last ten years and given the complete absence of consensus among the

authors, two independent schools use it as the core of their studies (Meynhardt,

2009; Rutgers, 2015).

The first school has its

roots in Moore’s Creating Public Value (1995), and it is centered on

Public Value Management. With an approach that ensures that public value is the

next step after the new public management, this result-oriented school moves

away from the state-versus-market perspective. On the other hand, Bozeman

(2002, 2007) opposes the concept of public values to the dominant economic

approaches for public policy analysis, focusing on and giving birth to the analysis

of public value failure. According to the author, the public values of the

society provide normative consensus about citizens’ rights and benefits,

obligations to the society and the state, and the principles on which

governments and policies are based (Bozeman, 2007, p.13).

Alternatively, there are

attempts to define public values by their differences to the public interest,

although circularity has been typically observed in these cases. On that

account, the concept of public benefit has also been discussed as a

tendency of recent literature to concentrate on which benefits people can take

from public actions (Alford and O’Flynn, 2008; Meynhardt, 2009; Rutgers, 2015).

Jørgensen and Bozeman

(2007) address two main points in the attempt to define public value: what the

values referred by the authors when they write about public values are; and

then, what issues should be analyzed. After an extensive literature review, the

authors have identified two central tendencies. The first one tackles the

recent public sector reforms as new public management practices or government

reinvention. The second – an emerging trend – focuses on former public values

of public administration, launching new progressive models, such as new public

governance or new public service.

After obtaining a sample

of 72 registered values, Jørgensen and Bozeman (2007, p.359) grouped different

concepts of public value, creating a structure in which citizens are in “the

environment”, and do not belong to the “society at large”. In this sense, the understanding

that citizens should be equal parts of a system is closely related to the core

concept of public value, summarized by Jørgensen and Bozeman (2007,

p.361), as the

“[…] idea

that the public sector should create or contribute to the common good and to

the public interest. Critics often call these concepts insubstantial and

worthless. What exactly does the common good or the public interest mean? […]

The public sector must not serve special interests, it must serve society as a

whole; the public sector is there for everybody, it is not the extended arm of

a particular class or group”. (Jørgensen and Bozeman 2007, p.361).

Several different

attempts were made to establish quantitative parameters for measuring the results

of the public sector activities. However, there are two distinct and

complementary criticisms to the performance measurement in the public sector.

The first one states that governments do not measure the right variables,

although they assess too many features. The second one points out a failure in

identifying long-term issues of the strategic planning of public entities.

According to this point of view, practices of performance measurement tend to

be broad and unfocused, which leads to an enormous failure to provide public

services (Atkinson, Waterhouse, and Wells, 1997; Chow, Ganulin, Haddad, and

Williamson, 1998; Modell, 2004).

In order to avoid these

mistakes, this analysis aims to measure the governance as the value perceived by

each Brazilian citizen, without any distinctions, through the compliance with

the existing laws for state-level public finance in Brazil, which have barely changed

since 2000. Thus, our attempt overcomes previous issues by measuring the best

variables available, as well as covering an extended time frame to identify

long-term matters of the strategic planning. The procedures are detailed in the

next section.

Methodology

Decision-making on

public expenditure and the necessary resources for governmental action are not a

merely economic matter, but a political one as well. They reveal a conundrum of

social forces developed by classes and shape the way a government will act. In

other words, “The budget is a mirror of the political life of a society, since

it registers and reveals which class […] pays more taxes, and which ones obtain

more benefits from the expenditure”, in a process that the society decides, via

their representatives, the goals for public expenditure and their corresponding

financial sources, and the methods for the effective control of actions (Oliveira,

2009, p.87).

According to Mikesell

and Mullins (2011, p.4), the budgetary process lies in the heart of politics.

Therefore, as the connections between technical and political aspects of

budgeting systems are not well defined, it is convenient to establish, as a

starting point, that the public sector did not change the function of the

budget in the last decades.

Budgetary data were collected

from the official websites of the legislative assemblies, government secretary

offices (Civil Office, Civil House or equivalent), planning secretaries, finance

departments (Treasury or equivalent), and from the official journals of the

states. Financial

data were collected from the National Treasury Secretary, from four

national databases – SISTN (Sistema de Coleta de Dados Contábeis dos Entes

da Federação), FINBRA (Finanças do Brasil), SICONFI (Sistema de

Informações Contábeis e Fiscais do Setor Público Brasileiro), and from the

Federal Treasury itself.

With 15 annual

observations between 2000 and 2014 for each one of the 27 federative units, the

variables collected and the corresponding sources are shown in Table 1, in

order to build a compound or multidimensional indicator.

A multidimensional

indicator gathers different units of analysis in one single measurement. It

uses a standardized method and ideally should allow a self-assessment. First,

we established how to set the weights for the indicator, which we called governance

intensity. After that, the scores were weighted up by the Brazilian population,

resulting in the governance incidence. At last, we determined the testing

conditions for reliability and internal consistency.

The concept of

governance intensity we used emerges from two different sources. The first one,

the Oxford Poverty and Human Development Initiative, uses the intensity concept

directly applied to poverty to measure the degree to which people are poor in

multiple dimensions, and not only to quantify the individuals that can be

considered poor. Mostly based on the Alkire-Foster method, we call governance intensity

the extent to which each state can be evaluated in five different dimensions.

In addition to that, the governance incidence estimates the proportion that the

intensity is observed across the country (Alkire, Foster, Seth, Santos, Roche,

Ballon, 2015).

Table

1 - Variables, sources, dimensions, divisions,

and scoring equations

|

Variable

|

Source

|

Dimension

|

Division

|

Scoring equations

|

|

Description

|

Weight

|

Description

|

Weight

|

|

|

Budget law enactment date

|

State budget laws

|

1 – Budget cycle regularity

|

0.2

|

-

|

0.2

|

|

|

Current revenue

|

Balance sheets

|

2 – Current budget balance

|

0.2

|

-

|

0.2

|

|

|

Current expenditure

|

|

Interest on debt

|

National Treasury Secretary

|

3 – Debt management

|

0.2

|

3.1 – Interest-to-expenditure rate

|

0.1

|

|

|

Consolidated net debt

|

3.2 - Consolidated net debt to Real Revenue

|

0.1

|

|

|

Real expenditure

|

4 – Planning accuracy

|

0.2

|

4.1 – Revenue accuracy

|

0.067

|

|

|

Real revenue

|

4.2 – Expenditure accuracy

|

0.067

|

|

|

Planned expenditure

|

State budget laws

|

4.3 – Surplus or deficit

|

0.067

|

|

|

Estimated revenue

|

|

Education expenditure

|

National Treasury Secretary

|

5 – Attendance to legal minimum percentage

allocations

|

0.2

|

5.1 – Education

|

0.1

|

|

|

|

|

|

|

|

Health expenditure

|

5.2 – Health

|

0,1

|

|

|

|

|

|

|

|

|

|

Using a method provided

by Decanq and Lugo (2008), this indicator had its dimensions equally weighted

at 20% each, making up the total weighting of 1, and not allowing negative

weights. Some of these dimensions were split again, keeping the criterion of equal

weights within each dimension. The equations in Table 1 equalize all scores in

order to generate values ranging from 0 to 1 in each dimension.

Taken from the annual budgetary

allocation and financial spending, the financial variables can reveal a pattern

of governmental response to the collective demand. Available data will be analyzed

under the perspective tested by Rubin and Willoughby (2009). The methods proposed

by them evaluate the practical use of the North American Financial Government

Performance Project (GPP), which consider four different evaluation criteria to

produce a grade for financial management.

The first dimension (A)

is the regularity of the budget cycle, as required by the article 34 of the

Federal Law 4.320/64 (Brasil, 1964). To obtain the ratings, every annual budget

law was awarded the maximum score, if the budget was enacted before the first

day of the fiscal year, January 1st. In case of delay, a reduction

of 1/365 per day was imputed.

The second dimension

(B), the balance of current budget, comprises the capacity of the states to

sustain current expenditures with current revenues of the same year, as specified

by the article 11 of the Federal Law 4.320/64. States that have fulfilled this

requirement received grade 1; those who have not were given decreasing rates,

according to the percentage of the revenue deficit.

The third dimension (C)

refers to the debt and comprises two divisions. The first one relates to the

payment of interest debts that were deducted from the maximum score, proportionally

to their impact on the total expenditure of the states. The second division of

the debt comprehends the ratio of current net debt to current net revenue of the

states. According to the Resolution 40/2001 of the Senate (Brasil, 2001), this

ratio should not exceed 2. Therefore, as the ratio approaches the maximum

limit, the scores tend to 0.

The fourth dimension (D)

is the accuracy of planning, subdivided into three equally weighted values,

according to the Annex 12 of the Federal Law 4.320/64. The first one (D1)

concerns the precision obtained when planning the expenditure. In this case, the

percentage of discrepancy between the planned and realized values is deducted

from the maximum score of 1. Similarly, the second condition (D2) is

applied to the accuracy of revenue. Finally, the accuracy between revenue and

expenditure (D3) makes up the third dismemberment of the accuracy planning.

The fifth dimension (E)

is defined as the constitutional minimum percentage of expenditure in education

(25%) and health (12%), represented by the divisions E1 and E2,

respectively. Compliance with the minimum value determines the maximum grade, while

non-compliance follows the highest score, proportional to the expenditure not

made in their functions (Brasil, 2000).

After using the

collected data in the corresponding equations, as described in Table 1, the

states obtained an annual score for each dimension, which scales the intensity

of the governance practiced.

Thus, the governance

intensity in each state can be determined annually by the Equation 1, wherein

each one of the values in the brackets represents the corresponding dimension

(or partition, in due cases) in Equation 2. They are detailed in Table 1.

After measuring the governance

intensity for each Brazilian state, the next step was to investigate how

citizens perceive this governance. The governance incidence is the result of

the weighted sum of the intensity. As weights, we determined the proportion of the

population living in each State, by year, as presented in Equation 3:

The underlying concept of

this intensity is the neutrality of the law, which refers to every citizen as

an equal part of the country. Thus, it is convenient to define the same weight

to each citizen, instead of ranking the states and verifying relative

advantages among them.

The reliability of the

indicator proposed was assessed via two measurements. In the first one, we

checked the internal consistency of the values obtained, by using a correlation

matrix for the indicator and its dimensions. The absence of correlation among

the dimensions revealed that they are independent of one another; while

correlations between the dimensions and the total governance intensity meant

that the components were significant. After checking the internal consistency,

the external validity was assessed by comparing the results to those provided

by the two previous attempts to measure subnational governance in Brazil, also using

correlation matrices. In the next section, the results of these procedures are better

detailed.

Results

Measuring the governance

intensity brought a deeper comprehension of public issues. The first dimension,

regularity of the budget cycle, revealed decreasing grades. Although the scores

might seem high – as the mean is still close to 1 – only six states rigorously followed

the legal schedule every year, and approximately 63% of the budget laws were

approved on time.

The results in Table 2

reveal that the budget enactments in the last year of the sample were one week

later in comparison with the first year. This decrease has two complementary

reasons. First, between 2000 and 2014, the budget enactment delay became, on

average, two days longer, when considering all states (scores of 0.987 and

0.981, respectively). Second, the number of states that started the fiscal year

with an enacted budget law dropped from 21 to 14, which represents 1 out of 3

states. In other words, more states were behind schedule, and the traditionally

late ones were even more delayed.

Several consequences

arise from the belated enactment of the budget law. Following a pattern

established at the federal level, most states use the previous year as the main

reference for cases in which the budget is not enacted on schedule. In these

conditions, states are allowed to spend only one-twelfth of the previous year’s

amount for non-compulsory expenses. As most representative functions are exempt

from this rule (including education and health), most investments and long-term

oriented policies face serious risk in this budget limbo.

The second dimension, the

balance of the current budget, comprises the capacity of the states to sustain

current expenditures with current revenues for the same year, as referred in

article 11 of Federal Law 4.320/64.

The superiority of the current

revenues over current expenditures showed the best scores of the entire sample.

Only seven states operated in deficit between 2000 and 2014. Paraná, Goiás,

and Piauí ran only one year in deficit (2000, 2001, and 2003,

respectively), while Minas Gerais (2001 and 2002) and Rio de

Janeiro (2012 and 2014) faced two years in deficit each. Furthermore,

the recent evolution of Rio Grande do Sul and São

Paulo urges a more in-depth analysis, since they hold the worst

performances for this dimension (3 years in deficit each).

The dangerous fiscal

condition of these two states could be easily verified through empirical means.

Among massive salary retains, civil servant strikes, and repression of student

movements against school closings, the executive actions taken by these states revealed

how critical their condition was in 2015.

Table 2 - Highlighted results of governance intensity

in Brazilian states, by dimension and divisions, in 2000-2014

|

Intensity, dimensions, and divisions

|

Variables

|

|

Mean Value

|

Higher averages (state)

|

Lower averages (state)

|

Best annual performance

(state:year)

|

Worst annual performance

(state:year)

|

|

Governance intensity

[(A+B+C+D+E)/5]

|

0.91

|

0.96 (AP)

|

0.85 (AL)

|

0.99 (AP: 2009)

|

0.72 (MA: 2000)

|

|

Dimension A – Budget cycle regularity

|

0.98

|

1.00 (AC, AM, MS, PE, PR, RS)

|

0.92 (ES), 0.94 (AL), 0.95 (RN)

|

1.00 (255 observations)

|

0.44 (ES:2003)

|

|

Dimension B – Current budget balance

|

0.99

|

1.00 (20 states)

|

0.98 (RS)

|

1.00 (392 observations)

|

0.88 (PR:2000)

|

|

Dimension C – Debt management

|

Dimension C

|

0.75

|

0.95 (AP)

|

0.49 (RS)

|

0.99 (AP:2008)

|

0.46 (AL:2002)

|

|

Branches

|

C1

|

0.97

|

0.99 (AP)

|

0.94 (RJ)

|

1.00 (RR:2012)

|

0.91 (SC:2012)

|

|

C2

|

0.54

|

0.92 (AP)

|

0.00 (RS)

|

0.95 (RN:2012)

|

0.00 (RS: 2000-2014)

|

|

Dimension D – Planning accuracy

|

Dimension D

|

0.91

|

0.96 (RS)

|

0.79 (RR)

|

1.00 (RS:2009)

|

0.52 (RR:2011)

|

|

Branches

|

D1

|

0.89

|

0.96 (RS)

|

0.73 (RR)

|

1.00 (BA:2007)

|

0.35 (RR: 2011)

|

|

D2

|

0.9

|

0.96 (RS)

|

0.79 (RR)

|

1.00 (RS:2012)

|

0.37 (DF:2003)

|

|

D3

|

0.95

|

1.00 (SP)

|

0.86 (RR)

|

1.00 (SE:2004)

|

0.46 (RR:2011)

|

|

Dimension E – Attendance to legal minimum percentage allocations

|

Dimension E

|

0.89

|

0.98 (SP)

|

0.76 (ES)

|

1.00 (CE:2001-2011)

|

0.38 (PE:2000)

|

|

Branches

|

E1

|

0.81

|

0.88 (SP)

|

0.42 (ES)

|

1.00 (CE: 2001-2011)

|

0.30 (PI:2008)

|

|

E2

|

0.96

|

1.00 (AC, AL, BA, DF, PR, RN)

|

0.83 (RJ)

|

1.00 (AC, AL, BA, DF, PR, RN: 2000-2014)

|

0.12 (MA:2000)

|

Note: The complete tables and results are

fully available upon request.

The government of São

Paulo issued the Decree n. 61.131 in February 2015 to cut 5% to 10% of

the then current expenditure, which provided some temporary relief. However,

the first project for the 2017 budget law brought an estimated revenue significantly

smaller than the expected.

Similarly, Rio Grande

do Sul reduced around 21% of its current use expenditure (São

Paulo, 2015; Rio Grande do Sul, 2015), but without achieving the same temporary

relief as São Paulo. Street protests and civil servant strikes anticipated the

Decree 53.303, which made official the financial calamity state, in November

2016.

The third dimension, the

debt, comprises two divisions. The first one relates to the payment of interest

debts, which were deducted from the maximum score, proportionally to their

impact on the total expenditure of the states. The second one is the ratio of

current net debt to current net revenues.

The allocation of

expenses for the payment of debt interest shows that, on average, states used

3.3% of their resources for this purpose. The annual evolution of the joint

performance of the states revealed significant improvement. From the initial average

of 4.4% of the expenditure in 2000, 2.3% of expenditure was used for paying the

interest in 2014. This decline can be explained by the lower interest rates nationwide,

better loan contracts, and extended payment deadlines, which together had a positive

impact on the debt issues. It is also worth highlighting the case of Roraima,

the only state to achieve a score of 1 (2002). This grade might be interpreted

as a data error or even as a refusal to paying interests, given the fiscal

condition of the state. However, Roraima had the second-best average

score on this criterion analysis, with an average of 0.9878 and standard

deviation of 0.0078, which makes the score reasonable.

The ratio of current net

debt to current net revenue of the states revealed great dispersion and high incidence

of minimum scores. These results indicate that the state debts should receive immediate

attention and action by the government planners. In the sample, 9 out of the 27

states exceeded the upper limit, including Mato Grosso, which surpassed

the limit only in 2000, and Rio Grande do Sul, which

did not reach the limit even once within the considered period.

However, results revealed

that, in general, the states have managed to reduce the ratio of debt to current

net revenue. All considered, the mean scores showed consistent improvement from

0.36 in 2000 to 0.65 in 2014. This fact raises the question whether the increase

in the debt-income ratio was more influenced by the growth in revenues rather than

by the decrease in debt. A brief analysis of the data shows that the revenues

increased faster than debt. This evidence is also consistent with findings that

states are now reducing the payment of interests, and that more recent

contracts have new deadlines, postponing the payments, but generating an

increasing future debt.

Equally weighted, the

two axes of the debt revealed no significant changes in the results observed in

each of its divisions. With regards to the joint analysis, it is worth

highlighting that the state of Rio de Janeiro has got the

second -and third- worst scores (0.4635 in 2002, and 0.4637 in 2003) of the

sample, but it was not among the states with the lowest average of indebtedness.

This fact occurred due to recurring scores higher than 0.5234 as of 2007

(including a maximum of 0.6132 in 2011), which considerably raised the average

value and resulted in a striking development in the recent years.

Regarding the planning

accuracy, the fourth dimension, Brazilian states got an average of 89.15% in

predicting the revenues. This value is slightly lower than the 90.13% accuracy

in planning the spendings, showing a balance inherent in the planning stages.

However, the revenues

and expenses observed got an average accuracy of 94.87%, revealing a higher assertiveness

in the execution steps, when compared to the planning stages. This verification

therefore reaffirms, at the subnational level, the hypothesis of greater managerial

freedom of the executive power to carrying out budgetary expenditures for both

cases of inaccuracy. Whether or not the revenues exceed the planned values, the

executive is allowed to increase the budget for existing expenses. If the government

faces insufficient income, discretionary cuts in expenditure can also be made

without prior legislative approval.

As for the last

dimension, the constitutional requirements for allocation were evaluated. For

this procedure, we used two sub-scores: one for education and another for

health funds. The minimum percentage allocated for education, in general, got an

average score in the order of 0.8120 for the states, with a deviation of

0.1483. Therefore, although the states usually do not meet the legal provision,

the high deviation denotes a wide variation within the sample. This result is

corroborated by the difference between the lowest and the highest averages of

the states. The states that showed the lowest average scores were Espírito

Santo (0.4171), Pernambuco (0.4786), and Mato Grosso

(0.6142). Espírito Santo was also responsible for two of the

three smallest annual allocations, getting a score of 0.4626 in 2011, and 0.44

in 2012. The highest score of 1 was obtained by 22 federative units at least

once, and the states of Ceará, São Paulo, Paraná, Amapá,

and Distrito Federal achieved the maximum annual grade at least five times

during the period assessed (11, 10, 8, 7, and 5 times, respectively).

The minimum application in

health resources showed superior results compared to those recorded in education.

All federal units obtained the maximum score at least once, and six of them (Acre,

Alagoas, Bahia, Distrito Federal, Paraná, and Rio

Grande do Norte) fulfilled the requirement throughout the

entire period assessed.

Two factors may explain

the difference between the minimum percentages. First, the mutual responsibility

of the different levels of contribution with the basic education, as determined

by the Brazilian law. The state-level government is not the only formally

responsible for providing and assuring quality in public schools. Therefore,

the low quality of the services offered due to the lack of resources might be

obscured by the responsibility shared with municipalities and the Federal

Government. Second, the obligatory expenditure percentage set for education is

much higher than that established for health (25% against 12%), which creates a

severe restriction, especially for states that have high costs with salaries and

debt interests.

With the results of the

minimum constitutional investments in education and health equally weighted,

the federative units of São Paulo, Acre, and Amapá showed

the highest average scores (0.9800, 0.9784, and 0.9707, respectively). Notwithstanding,

Ceará was the state that obtained the maximum score more times because

it met these minimum resources health and education for in 11 out of the 15 years

possible. The states with the worst average scores were Espírito Santo

(0.7651), Pernambuco (0.7856), and Mato Grosso (0.7926).

In addition, nine other states did not obtain the maximum score even once

during the evaluation period.

The overall results

reveal that considerable improvements were made outside the south and southeast

regions of Brazil. In this sense, Maranhão, Pernambuco, Goiás,

Paraíba, and Amazonas have accomplished the most in these fifteen

years. It is also worth mentioning that the enhancements are numerically more

significant than the decays. On one side, the states of Maranhão and Pernambuco

had increased 0.22 and 0.13 respectively; whereas Minas Gerais

and Acre got grades in 2014 worse than they did in 2000, with -0.048 and

-0.046, respectively.

The year 2010 revealed

itself as a turning point for most of the state governances, and it strongly affected

the economic scenario as a whole. Two explanations are possible for this

conundrum. The first one is the apex of the economic boom in Brazil, which made

it possible for the states to take advantages and improve their performance.

The second explanation is the end of the electoral cycle, with general

elections taking place in October 2010, and the elected politicians assuming

their position in January 2011. Unfortunately, the precise intensity of these

factors will have to be determined in future studies, due to the lack of a

longer series for analysis.

After assessing the governance

intensity, the scores were weighted by the population of each state to provide

the governance incidence. Table 3 shows that the first year of the series,

2000, holds the lowest value for governance incidence in the interval assessed.

This fact occurred mostly because of the extremely low debt scores, and the low

values of health and education allocations. In the following year, 2001, the

worst criteria for the states changed. Planning accuracy was even worse than

the constitutional requirements for financial allocation to education and health.

Meanwhile, the debt still got the lowest grade considering the states

altogether; it was even lower than in 2000.

Table 3

– Governance incidence weighted by the population of the Brazilian states in 2000-2014

|

Year

|

Population-weighted scores

|

|

Governance

incidence

|

Score A

|

Score B

|

Score C

|

Score D

|

Score E

|

|

2000

|

0.8681

|

0.9862

|

0.9934

|

0.5841

|

0.9077

|

0.8693

|

|

2001

|

0.8847

|

0.9881

|

0.9963

|

0.5711

|

0.9174

|

0.9507

|

|

2002

|

0.8797

|

0.9916

|

0.9958

|

0.5552

|

0.9332

|

0.9227

|

|

2003

|

0.8812

|

0.9795

|

0.9995

|

0.5693

|

0.9385

|

0.9193

|

|

2004

|

0.8807

|

0.9893

|

1.0000

|

0.5868

|

0.9384

|

0.8888

|

|

2005

|

0.8853

|

0.9882

|

1.0000

|

0.6129

|

0.9441

|

0.8813

|

|

2006

|

0.8836

|

0.9493

|

1.0000

|

0.6372

|

0.9438

|

0.8875

|

|

2007

|

0.8900

|

0.9534

|

1.0000

|

0.6698

|

0.9387

|

0.8881

|

|

2008

|

0.8991

|

0.9777

|

1.0000

|

0.6965

|

0.9261

|

0.8951

|

|

2009

|

0.9135

|

0.9905

|

1.0000

|

0.7123

|

0.9455

|

0.9192

|

|

2010

|

0.9065

|

0.9918

|

1.0000

|

0.7173

|

0.9321

|

0.8910

|

|

2011

|

0.9117

|

0.9885

|

1.0000

|

0.7346

|

0.9325

|

0.9026

|

|

2012

|

0.9088

|

0.9927

|

0.9900

|

0.7315

|

0.9359

|

0.8938

|

|

2013

|

0.8985

|

0.9884

|

0.9899

|

0.7383

|

0.9004

|

0.8754

|

|

2014

|

0.8958

|

0.9802

|

0.9838

|

0.7286

|

0.9158

|

0.8705

|

The subsequent years,

2001-2002, showed considerable improvement on the grades achieved, as shown in

Table 3. As a clear effect of the enactment of the Fiscal Responsibility Law,

the states increased their average scores in four out of the five dimensions

under analysis. The improvements, however, were not enough on the debt

dimension, which was still critical for the states’ performance during the entire

evaluation.

Testing of reliability and

validity

The indicator we now

propose holds a strong internal consistency, as shown in Table 4. We verified

positive correlations with all components individually, with a significance of 0.001.

This result implies that all components were relevant for the indicator as a

whole, as stated by the positive signal. Furthermore, two positive correlations

were found within the indicator dimensions. First, a weak positive correlation was

noticed between the current balance and the debt dimensions. In this case, further

works should check the causality direction, but it is theoretically and

empirically expected that a negative imbalance causes debt to increase.

Our results showed a

second positive correlation between the debt and minimum allocation in

education and health. In spite of this correlation being less significant

(0.05), governments should not neglect the harmful effects of the potential

trade-off between these two dimensions, since poor debt management can compromise

the obligations with the social policy in these areas. An alternative to

overcome this danger would be to enact mechanisms that ensure this minimum allocation,

even in high debt scenarios.

Table 4 - Correlation matrix: internal consistence

|

Intensity

|

A Scores

|

B Scores

|

C Scores

|

D Scores

|

E Scores

|

|

Intensity

|

1

|

|

|

|

|

|

|

A Scores

|

0.24***

|

1

|

|

|

|

|

|

B Scores

|

0.17***

|

-0.05

|

1

|

|

|

|

|

C Scores

|

0.83***

|

0.02

|

0.19***

|

1

|

|

|

|

D Scores

|

0.23***

|

0.04

|

-0.03

|

-0.09

|

1

|

|

|

E Scores

|

0.50***

|

0.05

|

-0.01

|

0.11*

|

-0.06

|

1

|

For the years 2004-2009,

the IGEB, developed by Miranda (2012), was used to establish a comparison,

while for 2010, we chose the IGovP, developed by Oliveira and Pisa (2015), was

taken as a reference. According to the results displayed in Table 5, the GI showed

a negative correlation with both of these indicators in Brazil, for the entire

duration of the assessment. The most extreme value of this correlation was

found with IGovP, which is consistent with our findings due to the lack of

quantitative reliability tests in the studies of Oliveira and Pisa (2015).

Table 5 - Correlation between GI and the previous governance

indices of the Brazilian states

|

Year

|

|

|

IGEB

|

IGovP

|

|

Correlation GI – Other indicators

|

2004

|

2005

|

2006

|

2007

|

2008

|

2010

|

|

-0.1557

|

-0.3082

|

-0.2981

|

-0.2976

|

-0.2579

|

-0.4321

|

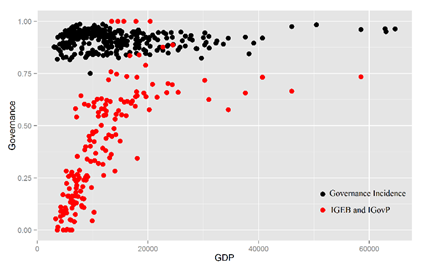

Thus, the plotted

indicators and the GDP per capita revealed distinct patterns. Figure 1 presents

the results for GI in black dots, which do not have a clear correlation with

the GDP. However, the red dots representing the results of IGEB and IGovP exhibit

a clear upward trend as the GDP increases. If the values on the extreme right

of the plot had been considered, this trend would have been even more evident.

Figure 1-Governance grades and GDP

The correlation values of

both groups reaffirm this evidence, as our indicator does not have a relevant

correlation with the GDP, showing a -0.07 value for the whole sample. On the

other hand, previous attempts have never found any annual correlating values below

0.70, or a mean correlation of 0.73 with the state GDP in the entire sample. In

other words, it should not be surprising that our results were so different

from the preceding ones, since the previous concept of governance essentially measured

just wealth.

Several considerations

arise from this difference. First, there is vast empirical evidence that

challenges IGovP and IGEB constructions as attempts to measure subnational governance.

In this sense, the choice of secondary indicators that led to an income-based

result could have widened the scope of governance to the point that the wealth

inequality condition in Brazil became evident through the analysis. Thus, our

choice to focus on public financial primary indicators became more independent

from inequality, establishing a new cutoff point between wealth and governance.

Second, it is possible

that a relation between wealth and governance, as wealthier governments are

more likely to have available resources to tackle governance issues. However,

the contrary is not valid, because poor governments do not have the same condition

due to the lack of governance requirements. Even in the wide scope of

governance assumed by IGEB and IGovP, the reality proves the opposite. Since none

of the Brazilian states have completely fulfilled the legal requirements for

public finance, we can speculate that some of them might be in worse condition

than others, and that the states that performed better did not do so by

increasing GDP.

Conclusions

This work presents the

formulation of a financial governance indicator for Brazilian states, by

establishing the theoretical weighting criteria and the corresponding grades, from

2000 to 2014. Despite the wide range of governance indicators that proliferate

every year, this one stands out for determining exclusively normative criteria,

based on an existing legal framework. Its potential application includes the

immediate use by the public administration as an instrument of verification, providing

citizens with an assertive mechanism for monitoring the government’s

performance, with nationally relevant specifications (Hood, 2012), and extensive

theoretical utilization in federal states.

The use of nationwide

stable updated criteria for measuring governance made possible its backward verification,

from the then current year to the implementation of the Fiscal Responsibility

Law in Brazil, thus building a consistent gap-free database of 15 years.

It would be possible to

establish a ranking of the states according to the scores they got. However, we

understand that such classification system does more harm than good, as the assignment

of relative positions might promote erroneous readings of relative success in the

face of a backdrop of poor general conditions. Thus, the scores were kept

according to the original grades, positively varying between 0 and 1, and the

possible ranking system was ignored.

The proposed indicator

led to results different than those of previous researches, which sought an

indicator for public governance, such as IGEB (Miranda, 2012) and the IGovP

(Oliveira and Pisa, 2015). Two factors caused this discrepancy. First, the

incorporation of variables not related to wealth. This choice was made due to criticism

on the use of GDP for the public sector performance analysis, either absolute

or weighted by population. The incorporation of GDP is not representative of the

government performance and may distort or mask results in inequality scenarios

(Tanzi, Schuknecht, 2000; Stiglitz, 2012; Atkinson, 2015). Thus, our evidence

shows that the distribution of the best results is barely correlated to the availability

of financial resources - typically in southeastern and southern states – as found

by previous works.

As an extension of the evidence

found, the adequacy of the proposed criteria for the conditions of the state

finances is beyond the scope of this study. Aspects such as the redesign of the

federal pact, the revision of the minimum constitutional percentages for social

expenditure, or the analysis of state revenue sources, though not yet addressed,

are intrinsically associated with this topic, and have crucial contributions to

further studies on subnational public finance in Brazil.

As restrictions of this

research, two factors must be taken into account. First, the complete lack of reliable

information concerning the real value of wages paid by the public sector made it

impossible to evaluate the performance of the fiscal responsibility law regarding

personnel expenditure. Second, the absence of a database on state budgets in

Brazil, which may cause some information to be unavailable in the future, or

dependent on the commitment of civil servants and politicians. So far, all the

information was open to the public, immediately or upon request. Therefore, we

hope that the Brazilian federal government will make the financial information accessible

in a more systematic format, in order to avoid inconsistencies due to the need for

searching through different databases throughout the years.

Another possible

extension of this article is the investigation of whether other developing

countries, with analogous administrative divisions, such as Mexico or Colombia,

also have similar legal requirements for subnational governments.

As a final remark, it is

relevant to mention that this research does not have tendencies towards any political

party, association or governmental plan. We do not propose a chase for an

optimal solution, but an a posteriori analytical tool to evaluate the

public sector performance. Finally, we also affirm that there are no existing

or potential conflicts of interest that would compromise the publication of

this study or future researches.

References

Alford, J.; O’Flynn, J. (2008). Public Value: A Stocktake of a Concept.

Twelfth Annual Conference of the International Research Society for Public

Management. Risbane: International Research Society for Public Management.

Alkire S, Foster J, Seth S, Santos MA, Roche JM, Ballon P. (2015).

Multidimensional Poverty Measurement and Analysis. Oxford: Oxford University

Press.

Atkinson A.J. (2015). Inequality: What Can Be Done? Cambridge:

Harvard University Press.

Atkinson AJ, Waterhouse JH, Wells RB. (1997). A stakeholder

approach to strategic performance measurement. Sloan Management Review, 38

(3), 25-37.

Bevir, M. (2010). Governance as Theory, Practice and Dilemma. In: The

Sage Handbook of Governance. Thousand Oaks: Sage.

Blaug R, Horner L; Lekhi R. (2006). Public value, politics and

public management. London: The Work Foundation.

Bozeman B. (2002). Public Value Failure: When Efficient Markets

may not do. Public Administration Review, 62 (2), 145-161.

Bozeman, B. (2007). Public Value and Public Interest:

Counterbalancing economic individualism. Washington: Georgetown

University Press.

Brasil.

Constituição da República Federativa do Brasil de 1988. Available

in: http://www.planalto.gov.br/ccivil_03/constituicao/constituicaocompilado.htm

Brasil.

1964. Lei nº 4320/1964. Diário Oficial da União, 04/05/1964.

Brasil.

2000, Emenda Constitucional nº 29. Diário Oficial da União, 14/09/2000.

Brasil.

2001. Resolução do Senado Federal nº 40/2001.Diário Oficial da União, 21/12/2001.

Brennan G, Buchanan JM. (1980). The Power to Tax: Analytical

Foundations of a Fiscal Constitution. Cambridge: Cambridge University

Press.

Chan JL., Xiao X. (2009). Financial Management in Public Sector

Organizations. In: Bovaird T, Loffler E (eds.). Public Management and

Governance, 2.ed. London: Routledge.

Chow CW, Ganulin D, Haddad K, Williamson J. (1998). The balanced

scorecard: a potent tool for energizing and focusing healthcare organization

management. Journal of Healthcare Management, 43(3), 263-280.

Constable S, Passmore E, Coats D. (2008) Public value and local

accountability in the NHS. London: The Work Foundation.

Decanq, K., Lugo, M.A. (2008) Setting Weights in Multidimensional

Indices of Well-Being and Deprivation. OPHI Working Paper n.18. Oxford: Oxford

Department of International Development.

Feldman M; Khademian AM. (2002). To Manage Is to Govern. Public

Administration Review, 62(5), 529–541.

Hobbes, T.(1998). The Leviathan. Oxford: Oxford University Press.

(Original work published 1651)

Hood, C. (2012). Public Management by Numbers as a

Performance-Enhancing Drug: Two Hypotheses. Public Administration Review,

72(S1), 585-592.

Jørgensen TB, Bozeman B. 2007. Public Values: An Inventory.

Administration & Society, 39(3), 354-381.

Kaufmann D, Kraay A, Mastruzzi M. (2011). The Worldwide Governance

Indicators: Methodology and Analytical Issues. Hague Journal on the Rule of

Law, 03 (2), 220-246.

Matthews F. (2012). Governance and State Capacity. The Oxford

Handbook of Governance, 281-293. Oxford: Oxford University Press.

Meynhardt, T. (2009) Public Value inside: what is public value

creation? International Journal of Public Administration, 32(3),

p.192-219.

Mikesell JL, Mullins DR. (2011). Reforms for Improved Efficiency

in Public Budgeting and Finance: Improvements, Disappointments, and

Work-in-Progress. Public Budgeting and Finance 31(4),1-30.

Miranda,

R.A. (2012). Governança: Um Índice para as Unidades Federativas Brasileiras (PhD

Thesis). Belo Horizonte: UFMG.

Modell S. (2004). Performance Measent Myths in the Public Sector:

A research note. Financial Accountability and Management, 20 (1),

39-55.

Moore MH. (1995). Creating Public Value: Strategic management

in government. Cambridge: Harvard University Press.

Moore MH. (2003). The Public Value Scorecard: A Rejoinder and an

Alternative to Strategic Performance Measurement and Management in Non-Profit

Organizations' by Robert Kaplan. Hauser Center for Nonprofit Organizations Working

Paper 18.

O’Donnell G. (2004). The Quality of Democracy: Why the Rule of Law

Matters. Journal of Democracy. 15(4), 32-46.

OECD, Organization for Economic Cooperation and Development. (2005). Modernising

Governance. Paris: OECD.

Oliveira,

F.A. (2009). Economia e política das finanças públicas no Brasil: um

guia de

leitura.

São Paulo: Hucitec.

Oliveira

AG, Pisa BJ. (2015). IGovP: índice de avaliação da governança pública -

instrumento de planejamento do Estado e de controle social pelo cidadão.

Revista de Administração. Pública, 49(5): 1263-1290.

Peters,

BG. (2012). Governance as Political Theory. In: Levi-Faur, D. The Oxford

Handbook of Governance, 19-32. Oxford: Oxford University Press

Rubin, M.M. Willoughby, K. (2009) Financial Management Grades for

the States: A Prospective Use. Public Budget and Finance, 29(1),

49-67.

Rutgers M.R. (2015). As Good as It Gets? On the Meaning of Public

Value in the Study of Policy and Management. American Review of Public

Administration, 45(1): 29-45.

Stiglitz, J. (2012). The Price of Inequality: How Today's

Divided Society Endangers Our Future. New York: W.W. Norton Company.

Stoker, G. (2006). Public Value Management: A New Narrative for

Networked Governance? The American Review of Public Administration, 36(1)

41-57.

Tanzi, V. (2008). The Role of the State and Public Finance in the

Next Generation. OECD Journal on Budgeting, 8(2): 1-27.

Tanzi V, Schuknecht L. (2000). Public Spending in the 20th

Century: A Global Perspective. Cambridge: Cambridge University Press.

Zumbansen P. (2012). Governance: An Interdisciplinary Perspective.

In: The Oxford Handbook of Governance. Oxford: Oxford University Press.

The full

list of the budget laws with the numbers and enactment dates is available upon

request.